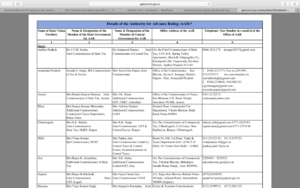

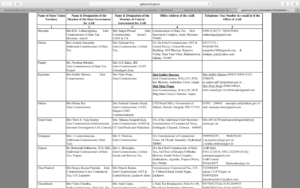

Advance Ruling Mechanism in GST

An advance ruling helps the applicant in planning his activities, which are liable for payment of GST, well in advance. It also brings certainty in determining the tax liability, as the ruling given by the Authority for Advance Ruling is binding on the applicant as well as Government authorities. Further, it helps in avoiding long drawn and expensive litigation at a later date. Seeking an advance ruling is inexpensive and the procedure is simple and expeditious. It thus provides certainty and transparency to a taxpayer with respect to an issue which may potentially cause a dispute with the tax administration. A legally constituted body called Authority for Advance Ruling (AAR) can give a binding ruling to an applicant who is a registered person or is desirous of obtaining registration. The advance ruling given by the Authority can be appealed before an Appellate authority for Advance Ruling (AAAR).There are time lines prescribed for passing an order by AAR and by AAAR.

The broad objectives for setting up a mechanism of Advance Ruling include:

- Provide certainty in tax liability in advance, in rela- tion to an activity proposed to be undertaken by the applicant;

- Attract Foreign Direct Investment (FDI);

- Reduce litigation;

- Pronounce ruling expeditiously in transparent and inexpensive manner;

“Advance ruling”means a decision provided by the Authority or the Appellate Authority to an applicant on matters or on questions specified in sub-section (2) of section 97 or sub-section (1) of section 100 of the CGST Act, 2017, in relation to the supply of goods or services or both being undertaken or proposed to be undertaken by the applicant.

The definition of Advance ruling given under the Act is a broad one and an improvement over the existing systems of advance rulings under Customs and Central Excise Laws. Under the present dispensation, advance rulings can be given only for a proposed transaction, whereas under GST, Advance ruling can be obtained for a proposed transaction as well as a transaction already undertaken by the appellant.

Charitable trust liable to pay GST in Maharashtra- AAR (Authority of Advance ruling)

Goods and services provided by charitable trusts for a consideration would classify as supply, making it liable for GST, the authority of advanced ruling (AAR) for GST in Maharashtra has ruled. ![]()

The ruling further states that trusts would need to register under GST if its annual turnover was above the threshold of Rs 20 lakh. The trust in its application argued that since its main activity was that of a charitable trust engaged in spreading religious knowledge by organising camps (satsang, shibirs), its ancillary activity of selling religious material in the forms of books, CDs, DVDs, pamphlets and statues shouldn’t be considered as business. #GSTonNGO#AAR#Wealth4India.